A comprehensive guide for homeowners and investors on understanding, calculating, and managing Philippine property tax obligations.

In the heart of every Filipino’s dream of building a home or investing in property lies a crucial aspect often overlooked until the last minute – property tax in the Philippines. As a vital component of property ownership in the Philippines, understanding and efficiently managing property tax can save homeowners and investors from unexpected financial burdens. At JCA Law Office Professional Corporation, we believe in empowering our kababayans with knowledge and insights to make informed decisions. Here’s a comprehensive guide to navigating property tax in the Philippines.

Understanding Property Tax in the Philippines

Property tax, or “Amilyar” as it is colloquially known, is a local tax imposed on the ownership of real property, including land, buildings, improvements, and machinery in the Philippines. Governed by the Local Government Code of 1991, this tax is a primary source of revenue for local government units (LGUs), supporting public services and community development projects.

How is Property Tax Calculated?

The amount of property tax you owe is determined by your property’s assessed value and the applicable tax rate set by your local government. The assessed value is a percentage of the market value, which varies depending on the property type. For instance, residential properties are typically assessed at a lower rate than commercial properties. The standard tax rate for cities and municipalities within Metro Manila is 2%, while it’s 1% for those outside the metropolitan area.

The Importance of Timely Payments

Timeliness in paying your property tax in the Philippines cannot be overstressed. Settling your dues before the deadline not only keeps you in good standing but also qualifies you for discounts in some LGUs. Conversely, late payments incur penalties, interests, and surcharges, adding to the financial strain. Remember, the local government has the authority to auction off properties with delinquent taxes, a situation every property owner wants to avoid.

Tips for Efficient Property Tax Management

Stay Informed: Keep abreast of the payment schedules and any changes in tax rates or policies in your locality. Ignorance is not bliss when it comes to tax obligations.

Avail of Discounts: Many LGUs offer early payment incentives. Take advantage of these discounts to save money.

Regularly Check Property Assessments: Ensure your property’s assessed value reflects its current state. If there have been significant changes, consider filing for a reassessment to prevent overpaying.

Consult Professionals: Navigating property tax laws and regulations can be complex. Seeking advice from legal and tax professionals can provide clarity and prevent costly mistakes.

JCA Law Office: Your Partner in Property Tax Management

At JCA Law Office Professional Corporation, we understand the challenges that come with managing property tax in the Philippines. Our team of experts is committed to providing you with personalized advice and solutions to ensure your property tax affairs are in order. Whether you’re a first-time homeowner, a seasoned investor, or somewhere in between, we’re here to guide you every step of the way.

Embrace the Filipino dream of property ownership with confidence and peace of mind. Let us help you navigate the complexities of property tax in the Philippines, so you can focus on what truly matters – building a secure and prosperous future for you and your loved ones.

For more information on how we can assist you with your property tax and other legal needs, message us today. Together, let’s make informed decisions for a brighter tomorrow.

Need Help with Philippine Property Tax?

JCA Law Office Professional Corporation assists Filipino-Canadians with property tax management, real estate transactions, and legal matters in the Philippines.

Navigating the Process of Selling Real Estate in the Philippines for Filipinos in Canada

A JCA Law Office specialty — combining legal expertise with a deep understanding of Filipino cultural values to guide you through cross-border real estate transactions.

At JCA Law Office Professional Corporation, we specialize in the intricacies of selling real estate in the Philippines, particularly for Filipinos residing in Canada. Our approach to these real estate transactions combines legal expertise with a profound understanding of the emotional and cultural nuances involved. We aim to provide comprehensive guidance in selling real estate in the Philippines, simplifying the legal process while respecting the deep cultural connections inherent in these significant decisions.

Understanding Emotional and Cultural Ties in Selling Real Estate

For Filipinos in Canada, selling property in the Philippines is more than a financial decision; it’s about managing a part of their legacy and cultural identity. Our team, deeply rooted in Filipino culture and values, offers not just legal expertise in selling real estate but also a sensitive understanding of the emotional ties involved, particularly in cases of inheritances or properties that hold sentimental value.

Expertise in Selling Real Estate Across Legal and Geographical Boundaries

Managing the sale of real estate in the Philippines from overseas presents unique challenges, such as navigating the legalities in two different countries and coordinating across time zones. Our team is adept at handling these complexities, offering tailored legal solutions for selling real estate in the Philippines that keep you well-informed and comfortable throughout the process.

Comprehensive Services for Selling Real Estate in the Philippines

Preparing your property in the Philippines for sale requires careful planning. We assist in enhancing your property’s appeal and suggest improvements that can increase its market value. Our team guides you through obtaining necessary documents like the Title Certificate, Tax Declaration, and Real Property Tax clearances, ensuring your documentation complies with Philippine law. We also provide insights into the latest trends in selling real estate in the Philippines, helping you position your property attractively for potential buyers.

Transparent Negotiations and Transactions in Real Estate Sales

Handling negotiations and transactions from afar can be daunting. When selling real estate in the Philippines, we represent your interests, ensuring transparency and fairness in all dealings. Our goal is to secure the best possible outcome for you, considering both financial and emotional aspects.

Navigating Tax Obligations and Legal Requirements in Real Estate Sales

Our services include advising on tax obligations such as Capital Gains Tax and Documentary Stamp Tax, ensuring that these are settled correctly when selling your real estate in the Philippines. We handle all legal aspects of the sale, providing peace of mind that every facet of the transaction complies with Philippine law.

Ensuring Smooth Title Transfer and Registration When Selling Real Estate

The transfer of ownership is a critical phase in the process of selling real estate. We meticulously oversee the drafting of the Deed of Absolute Sale, Special Power of Attorney, and Deed of Extrajudicial Settlement (for inherited property), submission for registration, and the entire title transfer process, ensuring accuracy and legal compliance.

Your Partner in Decisions of Selling Real Estate in the Philippines

JCA Law Office Professional Corporation is more than just a law firm; we are your partner in the journey of selling real estate in the Philippines, aligning our legal expertise with an understanding of Filipino values and culture. We are committed to making your real estate transactions as seamless and respectful of your heritage as possible.

Bridging Two Homes in Real Estate

For Filipinos in Canada looking to sell their properties in the Philippines, JCA Law offers a bridge between two homes, ensuring that the process of selling real estate is handled with care, professionalism, and cultural empathy. Contact us for comprehensive support and guidance tailored to the Filipino community in Canada.

Need Help Selling Property in the Philippines?

Our Filipino-Canadian lawyers specialize in cross-border real estate transactions. Let us handle the legal complexities while you focus on what matters most.

Navigating Real Estate Inheritance in the Philippines: Transferring Property Titles from Deceased Relatives

A comprehensive guide for Filipino-Canadian heirs on how to transfer property titles from deceased relatives in the Philippines, including legal requirements, tax obligations, and step-by-step procedures.

In the Philippines, a common occurrence is finding a property that remains titled under the name of a deceased relative, usually a parent or grandparent. Despite the death of the original owner, these properties often continue to be utilized, maintained, or even transacted by surviving heirs without the legal paperwork having been updated. This situation can create legal and financial complexities that may potentially jeopardize ownership rights and the value of the property.

If you are an heir to such a property, it is crucial to transfer the title officially to avoid future legal disputes and to ensure the proper valuation of your inheritance. Here, we will discuss the process, requirements, and potential challenges involved in transferring real estate titles in the Philippines from deceased relatives to their living heirs.

Understanding the Importance of Title Transfers

Property titles in the Philippines are legal documents that prove ownership over a piece of land or a building. When the owner of a property dies, the title does not automatically pass on to the heirs. Instead, it remains in the name of the deceased until the legal process of transfer is completed. This delay can lead to several problems:

Potential for Disputes: The property might be subject to inheritance disputes among the potential heirs, which could lead to lengthy legal battles.

Inability to Transact: The heirs may not be able to sell, mortgage, or lease the property since the title is still under the deceased’s name.

Tax Liabilities: The property may incur estate taxes and penalties that could diminish the value of the inheritance.

The Transfer Process: From Estate Tax Clearance to Title Transfer

The process of transferring a title from a deceased person to the living heirs involves several legal and administrative steps. These steps are generally as follows:

Step 1: Secure a Death Certificate

Obtain a certified copy of the death certificate from the local civil registry or the Philippine Statistics Authority (PSA).

Step 2: Probate of Will or Declaration of Heirs

If the deceased left a will, it must be probated, i.e., approved by the court. If there is no will, the court will have to issue a Declaration of Heirs.

Step 3: Payment of Estate Taxes

Calculate the estate tax due based on the value of the estate at the time of the owner’s death and pay this to the Bureau of Internal Revenue (BIR). This step involves filing the estate tax return and submitting the necessary documents.

Step 4: Secure a Tax Clearance

After paying the estate tax, secure a Certificate of Tax Clearance from the BIR, indicating that the estate tax has been fully paid.

Step 5: Judicial Partition or Extrajudicial Settlement of Estate

If the heirs cannot amicably decide on the distribution of the property, a court-supervised partition is necessary. If they agree, they can execute an Extrajudicial Settlement of Estate among themselves.

Step 6: Transfer of Title

Once the property has been properly partitioned or settled, the title can be transferred to the heirs. This requires filing a Deed of Adjudication with the Registry of Deeds, paying the corresponding transfer taxes, and obtaining the new titles under the heirs’ names.

Conclusion

Transferring a property title from a deceased relative in the Philippines to living heirs might appear to be a daunting task due to the number of steps and legal complexities involved. However, it is a critical process to prevent disputes and protect the value of your inheritance. It is advisable to seek legal counsel to help navigate through this process to ensure you adhere to all the requirements of the law, thereby ensuring a smooth and successful transfer.

Need Help with Philippine Property Inheritance?

JCA Law Office assists Filipino-Canadians with estate settlement, property title transfers, and extrajudicial settlements in the Philippines. Contact us for a consultation.

Mortgage Refinancing Guide for Filipino Homeowners in Ontario

Benefits, factors to consider, and how to get started with refinancing your Ontario mortgage.

Mabuhay, mga kababayan! For many Filipinos in Ontario, owning a home represents the achievement of a lifelong dream. As a homeowner, it’s essential to make informed decisions about managing your mortgage. Mortgage refinancing is one such option that can provide significant benefits, such as lower interest rates, reduced monthly payments, or debt consolidation. This guide will discuss mortgage refinancing for Filipino homeowners in Ontario and how to determine if it’s the right choice for you.

What is Mortgage Refinancing?

Mortgage refinancing involves replacing your existing mortgage with a new one, typically with more favorable terms. It’s an opportunity to renegotiate the interest rate, loan term, and other conditions of your mortgage, which can potentially save you money and make managing your finances easier.

Benefits of Mortgage Refinancing

Key Benefits

Lower Interest Rates — Refinancing may enable you to secure a lower interest rate, potentially saving you thousands of dollars in interest payments over the life of your mortgage.

Reduced Monthly Payments — With a lower interest rate, your monthly mortgage payments may decrease, allowing you to free up cash for other expenses.

Debt Consolidation — If you have high-interest debts, such as credit cards or personal loans, refinancing can help you consolidate them into a single, lower-interest mortgage payment.

Switching Mortgage Types — You may wish to change from a variable-rate mortgage to a fixed-rate mortgage, or vice versa, depending on your financial goals and market conditions.

Access Home Equity — Refinancing can enable you to tap into your home’s equity for expenses like home renovations, investments, or education costs.

Factors to Consider

Important Considerations

Closing Costs — Refinancing your mortgage comes with closing costs, such as legal fees, appraisal fees, and title insurance. Ensure you can recoup these costs through savings from refinancing before proceeding.

Prepayment Penalties — Some lenders charge prepayment penalties if you pay off your mortgage early. Check your mortgage contract and weigh these potential costs against potential savings.

Break-even Point — Calculate how long it will take to recoup the costs of refinancing through reduced monthly payments. Ensure the break-even point is within your intended time frame for staying in the home.

How to Get Started

Assess Your Financial Situation — Review your current mortgage terms, interest rate, and remaining balance. Determine your financial goals and consider how refinancing can help you achieve them.

Research Lenders — Shop around for lenders with competitive rates and terms. As a Filipino homeowner, you may want to consider working with lenders who understand and cater to the needs of the Filipino community.

Gather Documentation — Prepare the necessary documents, such as proof of income, credit reports, and home appraisal, to facilitate the refinancing process.

Consult a Mortgage Broker — A mortgage broker can help you navigate the refinancing process and find the best deal for your specific situation.

Conclusion

Mortgage refinancing can be an advantageous tool for Filipino homeowners in Ontario, offering the potential for savings and improved financial management. However, it’s essential to carefully weigh the benefits and costs before proceeding. By doing a thorough research and consulting with a mortgage broker, you can make an informed decision that best aligns with your financial goals.

Considering Mortgage Refinancing?

Our real estate lawyers can guide you through the refinancing process and protect your interests.

I remember when I was still a little kid, whenever my kindergarten teacher asked our class to draw during art time, I would always draw a house with a small picket fence, protecting the colorful flowers and grass, a big tree and probably a car. These images come to us as distant fantasies, usually at young tender ages, still untouched by the realities of the world. Innocent and filled with hope, we dream of our futures, bright-eyed and excited. As we grow older, we strive to get that dream job, buy that dream car, stroll around with that one true love and of course, purchase and own that dream house that we used to draw when we were young.

For most people, this will be one of the biggest decisions of their lives. Here in Toronto, purchasing a house will most likely be the most significant (and most expensive) decision you will ever make in your lifetime. There’s a lot of money on the line, not to mention the documents and legal papers that come with it.

It is therefore crucial that all bases are covered. This includes a basic understanding of real estate law and why real estate lawyers are needed in real estate transactions.

Real Estate Law Defined

The legal definition of real estate law, otherwise understood as real property, resides in the understanding of the land itself. This historic notion of property and law dates back to our earliest settlers and their desires to socially construct their settlements and the necessary divisions amongst inhabitants (arguably not much has changed). The real property extends also to what sits on the land, such as the house. Many factors are involved regarding the transferability of property. This is where it can get a little tricky and oftentimes necessary to have a lawyer by your side. Quite frankly, we cannot always trust who we are engaging with or take things as important as property/real estate, at face value. Lawyers can ensure that all loopholes are covered and that all details are agreed upon and communicated clearly to you.

Understanding The Real Estate Closing Process

Closing on property deals is the most crucial event in the purchase and sale transaction of real estate property, as this can be very confusing and complex both to the buyer and seller. It must be ensured that the deed and other closing papers are accurately prepared by someone who is knowledgeable and familiar with real estate closing law. This is a very detailed process and one cannot afford to miss any details.

Initially, I found it strange whenever I heard that people who were in the process of either buying, or selling real estate property here in Canada, were in need of a credible real estate lawyer. Back in my native country, the Philippines, lawyers are not really needed when you buy or sell a house. People would depend more on their real estate broker/agent/bank, and usually, the people involved (buyer and seller) know and have already met each other in person. The legal aspects are not given that much weight. Unlike here in Canada, people live in a fast-paced environment, all those involved in real-estate transactions know that it is important to ensure that all the financial decisions and monetary transactions are protected. This can all be found in the legal agreement.

Titles pass from seller to buyer, who then pays the balance of the purchase price. Usually, this balance is paid in part from the proceeds of a mortgage loan. A closing statement must be prepared prior to the closing, indicating the debits and credits to the buyer and seller. A real estate lawyer is often necessary in order to help you understand the nature, amount, and fairness of closing costs.

At the end of the day, you want to make sure that the deed and mortgage documents you will be signing are properly executed, and that you’ll have peace of mind after the closing process has been completed.

JCA LAW OFFICE has dedicated and knowledgeable lawyers who will gladly help you in your real estate closings (purchase and sale) and refinancing transactions. You may visit our main office at 168B Eglinton Ave. East, Toronto, ON M4P 1A6. We have another location right within the Philippine Consulate building at 160 Eglinton Ave. East, Suite 406, Toronto, ON M4P 3B5.

IMMIGRANTS IN CANADA WILL CONTINUE TO BOOST REAL ESTATE MARKET IN THE NEXT 5 YEARS

BY: GIN AGUILAR

Every year, more than 200,000 immigrants from different countries around the globe are being admitted and welcomed as new immigrants by the government of Canada. It should come as no surprise then that if the current international migration level remains the same, immigrants in Canada will continually boost the real estate market and are projected to acquire 680,000 homes over the next five years.

According to the Newcomer 2019 survey done by Royal LePage real estate company, newcomers to Canada make up 21 percent of homebuyers. For the said survey, “newcomers” have been described as persons who relocated to Canada within the last 10 years. Respondents consist of immigrants, refugees and people with a student or working visa. The average time spent in Canada by respondents is four years.

President and CEO of Royal LePage Phil Soper mentioned in a news interview with CBC’s Radio-Canada that “In addition to supporting Canada’s economic growth, newcomers to Canada are vital to the health of our national real estate market”. Soper also said that new immigrants represent between 2 to 3 million people, while the total Canadian population is approximately 37 million. “What was remarkable to us is just how many newcomers coming to Canada are focused on owning a home. Depending on the region of the country, almost all newcomers arrive with the necessary funds to purchase a home,” Soper further added.

The survey revealed that 86 percent of newcomers see real estate as a good investment. “It is not surprising that immigrants view owning a home in Canada as a good investment. Having lived abroad myself, I have seen first-hand the challenges of relocating a family to a different country. It takes courage and commitment. Newcomers are doing more than investing in Canadian real estate, they are investing in their family’s future,” Soper continued.

It is also important to note from the survey that upon arriving in Canada, 64 percent of newcomers prefer to rent, while 18 percent opt to live with family or friends to avoid high rental costs, and 15 percent purchase their own homes.

Recently, Canada has been ranked as the country with the highest quality of life and has always been included as one of the best countries in the world. The maple-leaf country is also known to have one of the most tolerant immigration policies in the world. It is, therefore, no wonder that most of the immigrants arrive with the needed knowledge, skills and capital because Canada is one of the top choices for skilled and capable people to live and settle with their families.

JCA LAW OFFICE has dedicated and competent Filipino-Canadian lawyers who will gladly help and ensure that your real estate closings (purchase and sale) and refinancing transactions will be smooth and stress-free. You may visit us at 168B Eglinton Ave. East, Toronto, ON M4P 1A6. We also have a satellite office conveniently located at 4th Floor Suite 406 of 160 Eglinton Ave. East, the same building where our Philippine Consulate office is currently located. We likewise have capable and hardworking licensed Immigration consultants to assist you regarding your immigration matters.

First-Time Home Buyer Programs in Ontario: Complete 2026 Guide for Filipino Newcomers

Last updated: February 7, 2026

Introduction: Why This Guide Matters for Filipino Newcomers

Buying your first home in Canada is one of the most exciting milestones for Filipino newcomers. After years of hard work, whether as a caregiver, healthcare professional, IT specialist, or in any other field, owning a home in Ontario represents stability and a brighter future for your family.

But the process can feel overwhelming. Between unfamiliar tax programs, complicated mortgage rules, and the sheer cost of housing in the Greater Toronto Area (GTA), many Filipino first-time buyers miss out on thousands of dollars in government incentives simply because they do not know what is available.

This guide breaks down every major program and incentive available to first-time home buyers in Ontario in 2026, with practical advice tailored specifically for Filipino newcomers. As of January 2026, the average home price in the GTA has dipped below million to ,289, making homeownership more accessible than it has been since 2021.

Quick Summary of Savings: A first-time buyer in Toronto purchasing a ,000 home could save a combined ,000 to ,000+ through the programs listed below, depending on eligibility. Read on to learn how to claim every dollar you are entitled to.

1. First Home Savings Account (FHSA) — The Newest Program

The First Home Savings Account (FHSA) is Canada’s newest tool for first-time home buyers, launched in April 2023. It combines the best features of an RRSP and a TFSA: your contributions are tax-deductible (like an RRSP), and your withdrawals for a home purchase are completely tax-free (like a TFSA).

How the FHSA Works

Feature

Details

Annual Contribution Limit

,000 per year

Lifetime Contribution Limit

,000

Carry-Forward Room

Up to ,000 of unused room carries to the next year

Tax Deduction

Contributions reduce your taxable income

Withdrawals for Home Purchase

100% tax-free (no repayment required)

Account Duration

Must close by the 15th anniversary of opening, or age 71, whichever comes first

Eligibility

Canadian resident, age 18+, first-time home buyer (not owned a home in the past 4 years)

Why This Matters for Filipino Newcomers

If you arrived in Canada recently, opening an FHSA should be one of your first financial steps. Even if you are not ready to buy a home yet, starting to contribute now means:

Immediate tax savings — every ,000 you contribute reduces your taxable income, saving you ,200 to ,000+ in taxes depending on your bracket

Tax-free investment growth — your money grows inside the account without any tax

Can be combined with the Home Buyers’ Plan (HBP) — use both FHSA and HBP for maximum savings

Pro Tip: If you opened your FHSA in 2025 but did not contribute the full ,000, you can carry forward up to ,000 of unused room to 2026. That means you could contribute up to ,000 in 2026 and claim a significant tax deduction.

2. Home Buyers’ Plan (HBP) — Withdraw from Your RRSP Tax-Free

The Home Buyers’ Plan (HBP) allows first-time home buyers to withdraw up to ,000 from their RRSPs to purchase or build a qualifying home, without paying tax on the withdrawal. If you are buying with a spouse or partner who also qualifies, you can each withdraw ,000 for a combined total of ,000.

Key HBP Rules for 2026

Feature

Details

Maximum Withdrawal

,000 per person (,000 per couple)

Repayment Period

15 years (starts 5th year after first withdrawal for 2022–2025 withdrawals)

Annual Repayment

1/15th of the total amount withdrawn each year

Eligibility

Canadian resident, first-time buyer (not owned a home in the past 4 years)

RRSP Holding Period

Funds must be in your RRSP for at least 90 days before withdrawal

Important: Unlike the FHSA, HBP withdrawals must be repaid to your RRSP over 15 years. If you miss a repayment, that amount is added to your taxable income for the year. Plan your repayments carefully.

FHSA + HBP: The Power Combination

You can use both the FHSA and the HBP for the same home purchase. Here is how a Filipino couple could maximize their savings:

Source

Person 1

Person 2

Total

FHSA (max over time)

,000

,000

,000

HBP (RRSP withdrawal)

,000

,000

,000

Combined Total

,000

,000

,000

That is up to ,000 in tax-advantaged funds for your down payment. For many Filipino families, this could cover a 20% down payment and avoid costly mortgage insurance entirely.

3. First-Time Home Buyers’ Tax Credit (HBTC)

The Home Buyers’ Tax Credit (HBTC) is a non-refundable federal tax credit that provides up to ,500 back when you file your taxes in the year you purchase your first home.

How It Works

Claim ,000 on line 31270 of your tax return

The credit is calculated at the lowest personal tax rate (15%), giving you up to ,500

You must be a first-time home buyer (have not owned a home in the past 4 years)

The home must be registered in your name (or your spouse’s name) and located in Canada

You must intend to occupy the home as your principal residence within one year of purchase

Easy to Claim: This credit is straightforward. When you file your taxes after buying your home, simply enter ,000 on line 31270. Your tax software will calculate the credit automatically. Do not forget this free ,500!

4. Ontario Land Transfer Tax Refund for First-Time Buyers

When you buy property in Ontario, you pay a provincial Land Transfer Tax (LTT) at closing. First-time home buyers can get a refund of up to ,000.

Ontario LTT Rates (2026)

Purchase Price Portion

Tax Rate

First ,000

0.5%

,001 to ,000

1.0%

,001 to ,000

1.5%

,001 to ,000,000

2.0%

Over ,000,000

2.5%

First-Time Buyer Refund

Maximum refund: ,000 (covers full LTT on homes up to ,000)

For homes over ,000: you still receive the full ,000 refund but pay the remaining LTT

Eligibility: Must be at least 18, a Canadian citizen or permanent resident, must move into the home within 9 months, and must never have owned a home anywhere in the world

How to apply: Your real estate lawyer applies for the refund at the time of closing

Example: Ontario LTT on a ,000 Home

Portion

Rate

Tax

First ,000

0.5%

,001–,000

1.0%

,950

,001–,000

1.5%

,250

,001–,000

2.0%

,000

Total Ontario LTT

,475

First-Time Buyer Refund

-,000

Net Ontario LTT Payable

,475

5. Toronto Municipal Land Transfer Tax Rebate

If you are buying in the City of Toronto, you pay an additional Municipal Land Transfer Tax (MLTT) on top of the provincial LTT. This effectively doubles your land transfer tax costs. However, first-time buyers can claim a rebate.

Current Toronto MLTT Rebate (2026)

Maximum rebate: ,475 (covers full MLTT on homes up to ,000)

For homes over ,000: you receive the ,475 rebate and pay the remaining MLTT

March 2026 Update — Expanded Rebate: Toronto City Council has approved an expansion of the first-time buyer MLTT rebate. Effective March 1, 2026, the rebate will provide the equivalent of a full rebate for first-time purchasers of residential properties valued up to ,000 (previously ,000). This is a major improvement that will save Toronto first-time buyers thousands of additional dollars.

Combined LTT Savings in Toronto (First-Time Buyer)

Tax/Rebate

,000 Home (Before March 2026)

,000 Home (After March 1, 2026)

Ontario Provincial LTT

,475

,475

Ontario First-Time Refund

-,000

-,000

Toronto MLTT

~,475

~,475

Toronto First-Time Rebate

-,475

-,475 (expanded)

Total LTT Payable

~,475

~,475

Total Savings from Rebates

,475

,475

Important for Toronto Buyers: If you are planning to purchase in Toronto, waiting until after March 1, 2026 to close could save you thousands in MLTT thanks to the expanded rebate. Talk to your real estate lawyer about timing your transaction.

6. GST/HST New Housing Rebate

If you are buying a newly built home (from a builder, not a resale home), you may be eligible for a GST/HST rebate. There are two programs to be aware of:

Existing GST/HST New Housing Rebate

Federal portion: Rebate of 36% of the GST paid, up to a maximum of ,300

Full rebate available for homes priced up to ,000

Rebate phases out between ,000 and ,000

No rebate for homes priced above ,000

Ontario portion: Additional rebate of 75% of the provincial portion of HST, up to ,000

NEW: First-Time Home Buyer GST/HST Rebate (Proposed)

Major New Incentive: The federal government has proposed a first-time home buyer GST/HST rebate that would eliminate the entire 5% federal GST on new homes valued up to million. This could mean savings of up to ,000 on a new build. The rebate phases out linearly between million and .5 million. This applies to agreements of purchase and sale entered into on or after May 27, 2025.

Note: The first-time home buyer GST/HST rebate is proposed legislation and has not yet received Royal Assent. The CRA will not process claims until the legislation is passed. However, if you are buying a new-build home, this is something to discuss with your lawyer.

7. CMHC Insured Mortgage — Buy with Just 5% Down

Many Filipino newcomers assume they need a 20% down payment to buy a home. That is not true. With a CMHC-insured mortgage, you can buy with as little as 5% down.

Minimum Down Payment Requirements (2026)

Purchase Price

Minimum Down Payment

,000 or less

5% of purchase price

,001 to ,499,999

5% of first ,000 + 10% of the remainder

,500,000 or more

20% (no CMHC insurance available)

Down Payment Examples

Home Price

Minimum Down Payment

Amount

,000

5%

,000

,000

5% + 10%

,000

,000

5% + 10%

,000

,289 (GTA avg.)

5% + 10%

,329

Key Benefits for First-Time Buyers in 2026

30-year amortization: First-time home buyers can now amortize their mortgage over 30 years (instead of the standard 25 years), lowering monthly payments

Insured mortgage price cap raised to .5 million: You can now use CMHC insurance for homes up to .5 million (previously million)

Lower stress test qualification: Insured mortgages often come with slightly lower interest rates

Did You Know? CMHC mortgage insurance is added to your mortgage balance and paid over the life of the loan. It is not an upfront out-of-pocket cost. This makes it much easier for newcomers to get into the market sooner.

8. Special Mortgage Programs for Newcomers

Canadian banks offer special mortgage programs designed specifically for newcomers who may not have an established Canadian credit history. As a Filipino newcomer, you should explore these programs:

Major Bank Newcomer Mortgage Programs (2026)

Bank

Program

Eligibility Window

Key Features

RBC

Newcomer Mortgage

PR within 12 months; Work Permit within 48 months

As low as 5% down; limited credit history OK; foreign income considered

TD

New to Canada Mortgage

PR within 5 years; Work Permit within 2 years

3+ months Canadian employment; flexible credit requirements

CIBC

Newcomer Mortgage

PR within 5 years; Work Permit 12+ months

Limited credit history OK; Canadian income required

Scotiabank

StartRight Program

PR or Temporary Resident within 5 years

Down payment must be from own funds (no gifts); credit building tools

BMO

NewStart Program

PR within 5 years; Work Permit holders

130-day rate hold (longest among big banks); flexible qualifications

Tips for Filipino Newcomers Applying for a Mortgage

Get pre-approved early: Even before you start house hunting, get a mortgage pre-approval. This tells you exactly how much you can afford.

Build Canadian credit fast: Get a secured credit card, use it for small purchases, and pay it off in full every month. Even 3–6 months of credit history helps.

Gather your documents: Have your employment letter, pay stubs, bank statements, and proof of down payment ready. If you have a 35%+ down payment, you may qualify without Canadian credit history.

Consider bringing 35% down: With a 35% down payment, RBC and other banks may approve your mortgage with minimal Canadian credit or employment history. This is especially useful if you are transferring savings from the Philippines.

Shop around: Do not just go to one bank. Compare rates from at least 3 lenders, including a mortgage broker who can access rates from multiple lenders.

9. Step-by-Step: Buying Your First Home in Ontario

Here is a simplified roadmap for Filipino first-time home buyers in Ontario:

Step 1: Get Your Finances in Order

Open an FHSA and start contributing

Build your credit score (aim for 650+)

Save for your down payment (minimum 5%, ideally 20%)

Budget for closing costs (typically 1.5–4% of the purchase price)

Step 2: Get Mortgage Pre-Approval

Visit your bank or a mortgage broker

Ask about newcomer mortgage programs

Get a pre-approval letter (typically valid for 90–130 days)

Step 3: Find a Real Estate Agent

Choose an agent familiar with your target neighbourhoods

Filipino-speaking agents may help with communication if needed

Your agent will help you search, negotiate, and submit offers

Step 4: Make an Offer and Negotiate

Submit an Agreement of Purchase and Sale (APS)

Include conditions: financing, home inspection, lawyer review

Pay a deposit (typically 5% of the purchase price, held in trust)

Step 5: Hire a Real Estate Lawyer

Your lawyer reviews the Agreement of Purchase and Sale

Conducts title search and ensures the property is free of liens

Handles land transfer tax payments and applies for first-time buyer refunds

Registers the property in your name on closing day

Step 6: Fulfill Conditions

Complete home inspection

Finalize mortgage approval with your lender

Arrange home insurance (required by your lender)

Waive conditions once everything is satisfactory

Step 7: Closing Day

Your lawyer handles the transfer of funds and documents

You sign mortgage documents and title transfer

Pay closing costs (land transfer tax minus rebates, legal fees, adjustments)

Receive your keys

Typical Closing Costs Breakdown

Cost Item

Estimated Amount

Land Transfer Tax (Ontario)

Varies (see calculator above)

Toronto MLTT (if in Toronto)

Varies (see calculator above)

Legal Fees

,500–,500

Title Insurance

–

Home Inspection

–

Appraisal Fee

– (sometimes covered by lender)

Property Tax Adjustment

Depends on closing date

Utility Connection Fees

–

Moving Costs

–,000

10. Common Mistakes Filipino Newcomers Make When Buying a Home

After helping many Filipino clients with their real estate transactions, we have seen some common mistakes that first-time buyers should avoid:

Mistake 1: Not Opening an FHSA Right Away

Many newcomers do not know about the FHSA or delay opening one. Every year you wait is ,000 in tax-deductible contribution room you cannot get back. Open an FHSA as soon as you arrive in Canada, even if buying a home is years away.

Mistake 2: Not Claiming the Ontario LTT Refund

Some buyers do not realize they qualify for the ,000 provincial refund (and the ,475+ Toronto rebate). Your real estate lawyer should handle this at closing, but make sure you confirm it. At JCA Law Office, we always ensure our clients receive every rebate they are entitled to.

Mistake 3: Sending Money from the Philippines Without Proper Documentation

If family members in the Philippines are gifting you money for your down payment, you need a signed gift letter confirming the funds are a gift (not a loan). Your lender will also want to see the paper trail of funds entering Canada. Keep all wire transfer receipts and bank statements.

Mistake 4: Buying More Home Than You Can Afford

Just because the bank pre-approves you for a certain amount does not mean you should spend that much. Factor in property taxes, utilities, maintenance, and your existing obligations (such as sending money to family in the Philippines). A general rule: your total housing costs should not exceed 30–35% of your gross household income.

Mistake 5: Skipping the Home Inspection

In competitive markets, some buyers waive the home inspection to make their offer more attractive. This is risky. A inspection could save you tens of thousands in unexpected repairs. Always include an inspection condition in your offer if possible.

Mistake 6: Not Hiring a Real Estate Lawyer Early Enough

In Ontario, you must have a lawyer to complete a real estate transaction. Do not wait until the last minute to find one. Engage your lawyer before you start making offers so they can review your Agreement of Purchase and Sale and advise you on any red flags.

Mistake 7: Not Understanding the Difference Between Freehold and Condo

Many Filipino newcomers come from the Philippines where condominiums are popular but work differently. In Ontario, condo ownership means paying monthly maintenance fees on top of your mortgage. These fees can be –,000+ per month. Always factor condo fees into your budget and review the condo’s status certificate before purchasing.

11. Complete Summary: All First-Time Buyer Incentives at a Glance

12. How JCA Law Office Can Help with Your Real Estate Closing

JCA Law Office Professional Corporation has extensive experience helping Filipino newcomers complete their real estate transactions in Ontario. As a firm that understands the unique needs of the Filipino-Canadian community, we provide:

Complete real estate closing services — from reviewing your Agreement of Purchase and Sale to handing you your keys

Land transfer tax rebate applications — we ensure you receive every dollar of the Ontario and Toronto first-time buyer refunds

Title search and insurance — protecting your investment from title defects and fraud

Mortgage documentation — coordinating with your lender to ensure a smooth closing

Guidance on all first-time buyer programs — we help you understand which incentives you qualify for

Tagalog and English service — clear communication in the language you are most comfortable with

Ready to Buy Your First Home in Ontario?

JCA Law Office Professional Corporation is here to guide you through every step of your real estate closing. We proudly serve the Filipino-Canadian community across the Greater Toronto Area.

Call us today: (647) 243-2286 Email: info@jcalaw.ca Office: Scarborough, Ontario (serving all of the GTA)

Yes. You can withdraw from both your FHSA and your RRSP (through the Home Buyers’ Plan) for the same home purchase. This gives you access to up to ,000 per person (,000 per couple) in tax-advantaged funds.

I just arrived in Canada. Do I qualify as a first-time home buyer?

Generally, yes. Most programs define a first-time buyer as someone who has not owned a home (or had a spouse/partner who owned a home) in the past 4 years. If you never owned property in Canada, you likely qualify. However, the Ontario LTT refund requires that you have never owned a home anywhere in the world. If you owned property in the Philippines, you may not qualify for the Ontario LTT refund, though you may still qualify for other programs.

Can I use money from the Philippines as my down payment?

Yes, but you need to properly document the source of funds. Keep records of wire transfers, bank statements showing the funds in your Philippine account, and a gift letter if the money is from family. Your lender will want a clear 90-day paper trail of where the funds came from.

Do I need a lawyer to buy a home in Ontario?

Yes. Unlike some countries, Ontario requires a lawyer to complete real estate transactions. Your lawyer handles the title search, land transfer tax, mortgage registration, and transfer of funds. This is not optional — it is a legal requirement.

What credit score do I need to buy a home?

Most lenders require a minimum credit score of 600–650 for insured mortgages. However, newcomer mortgage programs from major banks (RBC, TD, CIBC, etc.) may be more flexible if you have been in Canada for less than 5 years. If you have a 35% down payment, some lenders will approve you with minimal credit history.

How much are closing costs in Ontario?

Budget for approximately 1.5% to 4% of the purchase price for closing costs. This includes land transfer tax (minus any rebates), legal fees (,500–,500), title insurance (–), and other adjustments. For a ,000 home, expect ,000 to ,000 in closing costs after first-time buyer rebates.

This guide is for informational purposes only and does not constitute legal advice. Tax laws and government programs are subject to change. Please consult with a qualified lawyer and financial advisor for advice specific to your situation. Information is current as of February 2026.

There are multiple steps in the home selling process and I will give you 6 steps to do so. Whether it’s a for sale by owner or you are about to hire a listing agent. Certain steps can vary from province to province, but this article will be a general guide. Be sure to check in with a local professional to confirm if any specific requirements apply to your area.

Here are some steps that will help with selling a house

STEP 1: find out how much your home is worth.

A big mistake that sellers make is often overpricing their home. Make sure to put it up for a reasonable price and consider whether the offer is hot, cold, or just right. Keep it in line with the older homes that have been sold in a comparative market analysis report.

STEP 2: Choose a listing agent.

A listing agent is a real estate broker who will represent you in the sale of your home. They will give you information on how to sell your house and will look out for your best interests. Try to hire experience.

STEP 3: Get your home ready.

Prepare your home for sale by decluttering and cleaning it. Think about hiring a professional to prepare your home for house showings or you could ask your agent for help. You could rent some new furniture, or you could just use your own. Remember that you only got one chance to make a good first impression, so be presentable.

STEP 4: Market your home.

You and your agent should decide the best way to advertise your home. Approve of your agent’s marketing strategy or figure out how to advertise and sell your home yourself. Hire a professional to take pictures of your house, or put up a virtual tour online for other people to see.

STEP 5: Show your home.

Remember that your house will be better to show if you sell during the warm weather rather than winter. Selling your home during the holidays will likely result in a lower sales price. Be ready for an open house and ask for feedback, you could then adjust the price, condition, and the marketing if needed.

STEP 6: Offers and negotiation.

Be prepared to have a lot of offers if your home is at a reasonable price. Don’t ignore any offers, even the lowball offers. Instead, negotiate using a counter offer. A real estate counteroffer occurs when a home seller and the buyer comes to terms that are not agreeable.

These are just some ways that will bring you one step closer to selling your house.

For more information about real estate, JCA Law Office can help.

Houses in Toronto could be difficult to maintain and organize. You may need to consider decluttering.

I used to be so organized, but there are moments that organizing is a hard thing to do.

Have you experienced that after traveling or came from vacation, you have some things or new things you bought from the places you were visited? If you are frequent travelers, the new stuff keeps filing and adding up.

After I unpacked the things from my journey, I began organizing things and removing unnecessary items floor by floor. At first, it was so easy until I have visited places frequently the question of decluttering begins.

Another decluttering lesson was right after my divorce and a few weeks that I decided to move to another place or apartment. And I was facing bankruptcy; a severe financial debt was started to trouble me. Soon I found a financial advisor to help me how to lessen my debts. To cut the story short, I decided to move from a one-bedroom apartment to a single room. How could I compress my things now? From the more prominent to smaller place.

As I collected my belongings for a second, I made a system to help me decide what to keep and what to throw. It worked effectively for me. Maybe it could work for you too.

The clutter scale 1-5. Number Five (5) being an essential scale.

5 – Important items that are priceless and non-negotiable. That includes family pictures, business documents, and office equipment.

4- Items that are being used daily. This pile includes clothing, furniture, and pieces of jewelry.

3 – Items you use on special events or barely used.

2 – Items you rarely use but refuse to throw away.

1 – Items you never use or items that are non-beneficial like old boxes, old clothing, computer equipment, and old electronics

As you sort your less important items. Ask yourself the following questions:

Do I enjoy it?

Is there a unique story behind it?

Will I have the space for it?

Will I be able to replace it?

Can I quickly borrow it or rent it if I need it again?

Do they help with future goals?

Does it compare to the items that are on top of my list?

The clutter scale is an effective way to get back in touch with your priorities. My priority at the time was to get rid of anything that will not help me in the long run.

Using the clutter scale, I learned to organize my life and my possessions based on values.

As you declutter your items, take a few minutes to think about your goals and priorities. You’ll find your home more memorable and efficient.

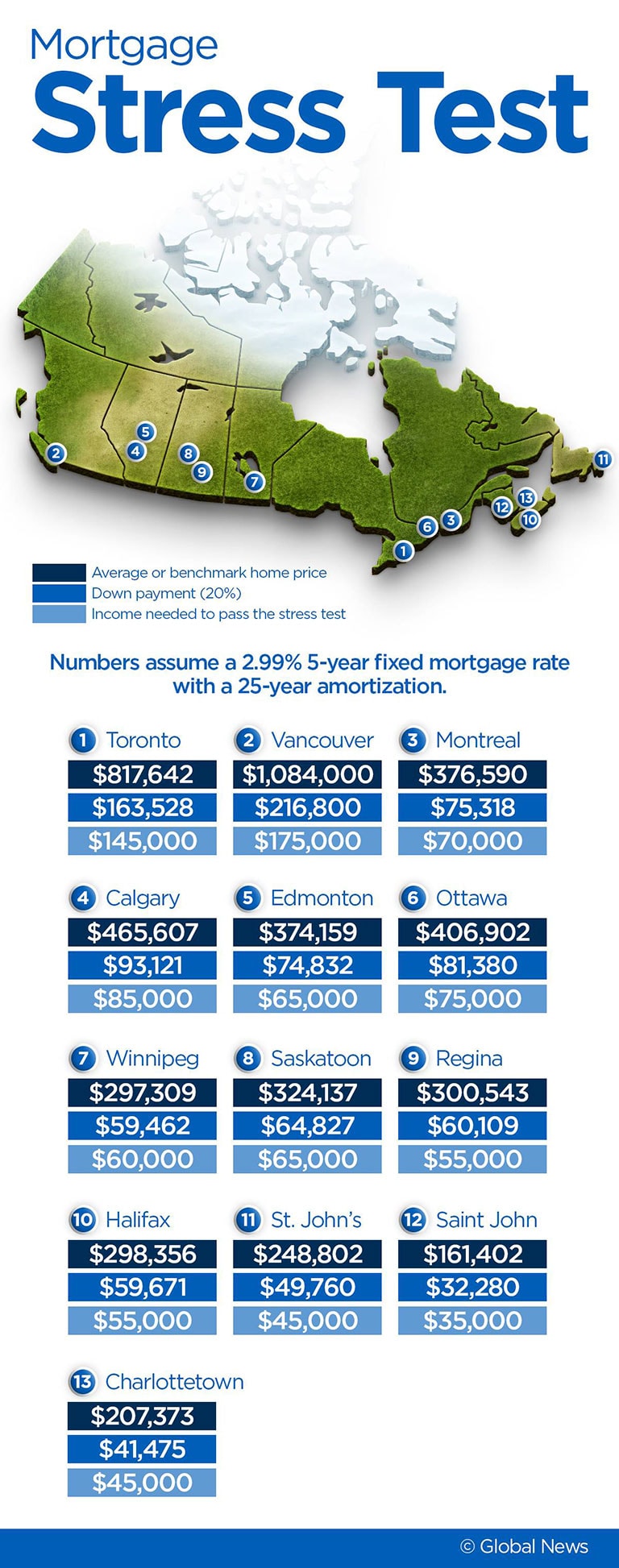

Numbers Assume a 2.99% 5-Year Fixed Mortgage Rate Wth a 25-Year Amortization.

The average price of a home in Canada is $491,000 according to the Canadian Real Estate Association (CREA).

And if you take out Toronto and Vancouver, the national average is slipped to 2% in the last 12 months. Under the new Mortgage Stress Test, target buyers now have to prove that they will be able to catch up with their bills even if their mortgage rate rose to .02 points.

In Toronto and Vancouver, Canada’s two most expensive markets, people are now turning to another less pricey condo and townhomes due to stricter mortgage rules. So, how much and what is the average income these days to qualify for a loan to buy an average-priced house in Canada’s largest cities?

Based on the mortgage affordability calculator from the site Ratehub.ca, here are the numbers we got, see the image on the left side.

What are the things do I need to consider before engaging to real estate or mortgage?

I was thinking to buy a house, and I have so much thinking and planning to consider. I need to assess myself if I could afford it and layout all the possible worst-case scenario in case something happened due to a loss or unforeseen expenses. It is like gearing-up when it is cloudy and buying travel insurance when considering a long trip or vacation. It is the same way taking a mortgage or real estate.

Is it necessary to assess mine before buying a house?

The OSFI introduced new and tighter rules for requiring borrowers with uninsured mortgages.

The Office of the Superintendent of Financial Institutions (OSFI) introduced new, tighter rules, requiring borrowers with uninsured mortgages (those putting a down payment of 20 percent or more) to undergo a stress test. As of Jan. 1, 2018, uninsured borrowers must now qualify as a new minimum rate — the greater of the Bank of Canada’s five-year benchmark rate, which currently sits at 4.99 percent, or 200 basis points higher than their mortgage rate.

While the stress test aims at ensuring that borrowers can afford mortgage rate hikes, some sources are questioning — if not outright opposing — the latest mortgage rule.

How the stress test works?

A stress test is a way of determining exactly how much you could afford and under what scenario or twist of unexpected events like my income has been reduced due to job loss. Could I still afford to take a mortgage or monthly payment? What if the interest rate in the market spike-up? Do you think I could afford to refinance my home?

This type of planning is very crucial for a few reasons. First, the interest rate is on the rise. So, too are the mortgages. According to the Canadian Real Estate Association, the national average home price was $496,500 in December 2017 with a year-over-year increase of 5.7%

If I could still afford to pay my home in the case of interest spike per year, then I could start shopping and re-evaluate my budget.

Due to new housing loan rules that came into effect last January 1, 2018, all homebuyers are required to get either the high-ratio mortgage or an uninsured mortgage are now subject to mortgage stress test and we should be qualified at a rate that is higher than I can pay.

The minimum qualifying rate (or stress test) for consumers getting uninsured mortgages– borrowers with a down payment of 20% or more– will be the greater of the Bank of Canada’s five-year benchmark rate (presently 4.89%) or 200 basis points above the mortgage holder’s contractual mortgage rate.

I may need to weigh my options; Do I save enough for higher down payment and defer the price of my real estate property or house? Or simply choose the more affordable home?

The real estate team of JCA LAW OFFICE could help you.

Only you could know the best answer based on your income status. It is still the best idea to talk to the expert in real estate closings like JCA Law Office if you want to consider buying a home.

On behalf of JCA Law Office on Friday, July 20, 2018.

Until this year, homebuyers needed to buy mortgage insurance if they could only afford to pay between five and 20 percent of the price of the property in their down payment. Only these homebuyers had to pass the stress test before they would get a mortgage. Now the rules have changed.

After January 1, almost all homebuyers began taking stress tests to see if they could afford the mortgage payments to buy a condo or house. Failing the test means that many homebuyers must buy a smaller home than they wanted – or not get a mortgage from banks and credit unions.

The Bank of Canada estimates 10 percent of borrowers who can make a down payment of 20 percent or more of the property’s cost will still not be able to secure a mortgage.

How the Stress Test Works

The stress test increases the interest rate that a homebuyer would be charged by two percentage points above either of the below, whichever is greater:

the Bank of Canada’s five-year benchmark lending interest rate; or

the current interest rate the lender charges for mortgages,

If a bank charges a five percent interest rate for mortgages, the bank calculates whether or not the homebuyer could pay the mortgage payments if the interest rate was seven percent, not five percent.

For example: assume that

the homebuyer wants a 25-year amortization period for their mortgage and

can make a down payment of 20 percent of the purchase price.

Then, possible mortgage payments are calculated at current interest rates:

under the old rules, the homebuyer must make $500 in monthly mortgage payments for every $100,000 of mortgage debt; but

under the new rules, the homebuyer must to able to pay $600 a month for every $100,000 in mortgage debt – even if the actual monthly payment is only $500 a month per $100,000 of mortgage debt.

How the Stress Test Result Can Change A Lender’s Decision About A Mortgage

Lenders decide how much a homebuyer can afford based on two ratios: the Gross Debt Service (GDS) ratio and the Total Debt Service (TDS) ratio.

The Gross Debt Service ratio is the percentage of pre-tax income that

a home buyer needs to pay their mortgage payment plus the monthly cost of property taxes, divided by their gross monthly (pre-tax) pay; or

a condominium buyer needs to pay the mortgage payment plus half of their monthly condo fees and the heating costs, divided by their gross monthly (pre-tax) pay.

If this ratio is less than 32 percent, most lenders will consider granting a mortgage. Lenders then consider the Total Debt Service ratio.

The Total Debt Service ratio is the percentage of pre-tax income that is needed to pay a homebuyer’s monthly debts, including credit cards, lines of credit, car loans and any other debts. The monthly mortgage payment is then added to the payments for these debts. The lender will probably grant a mortgage if the TDS is 42 percent or less of a homebuyers gross monthly income.

The stress test increases the mortgage payment amount when the GDS and the TDS are calculated. A home buyer would not get a mortgage if the amount added to the mortgage payment pushes the ratios above the GDS’ 32 percent and the TDS’ 42 percent limits.

What To Do When A Homebuyer Fails The Test

A homebuyer has two choices:

Buy a cheaper home. This lowers the amount of the mortgage payments so that the homebuyer passes the stress test.

Borrow from an alternative lender. These are smaller financial companies that the government does not insure. These lenders charge a much higher interest rate (eight to 11 percent) than banks do, as their risk is higher if the homebuyer defaults.

If interest rates climb further, still more people will see their chances of owning one’s own home fade because of the stress test.